Why Today’s Foreclosure Numbers Don’t Signal Another 2008 Crash

- WWH

- May 15

- 3 min read

You’ve probably seen headlines lately claiming that foreclosures are increasing, and for many people, that immediately brings back memories of the 2008 housing crash. That reaction makes sense. The foreclosure wave during that time left a lasting impression, and no one wants to experience a market collapse like that again.

But today’s market conditions are very different from what they were back then. Here’s why.

Foreclosures Are Increasing — But Context Matters

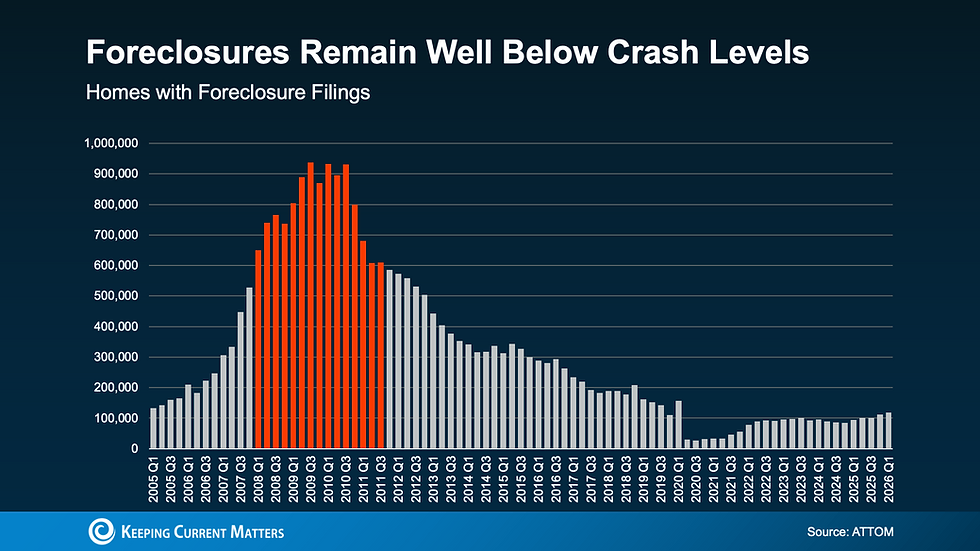

According to ATTOM, foreclosure filings are up 26% compared to last year, and filings have risen for five consecutive quarters. While that may sound alarming at first glance, the bigger picture tells a much different story.

What we’re seeing right now is more of a return to normal market activity rather than the beginning of a housing crisis.

One important thing to remember is that foreclosure activity during 2020 and 2021 was unusually low because of government protections and foreclosure moratoriums introduced during the pandemic. Those years were never considered “normal” market conditions.

When you compare today’s foreclosure numbers to the years just before the pandemic — like 2017, 2018, and 2019 — filings are still lower than they were during a typical housing market. That means today’s levels remain below historical averages and nowhere near what happened during the 2008 crash.

Even with the recent increase, foreclosure activity is still far from crisis territory.

Homeowner Equity Is a Major Difference

One of the biggest reasons today’s housing market looks nothing like 2008 is homeowner equity.

Back during the housing crash, many homeowners owed more on their mortgages than their homes were worth. Selling wasn’t an option for many people, leaving foreclosure as the only path forward.

Today, most homeowners are in a completely different financial position.

According to Cotality, the average homeowner currently has around $295,000 in equity. That equity gives homeowners more flexibility and more options if they run into financial hardship.

Instead of losing their home to foreclosure, many homeowners today can sell their property, pay off what they owe, protect their credit, and in many cases still walk away with money from the sale.

That’s a major reason experts aren’t expecting foreclosures to spiral the way they did during the last housing downturn.

Not Every Foreclosure Filing Ends in Foreclosure

Another important detail many headlines leave out is that a foreclosure filing doesn’t automatically mean someone will lose their home.

Data from ATTOM shows that completed foreclosures remain significantly lower than total foreclosure filings and foreclosure starts. Many homeowners are able to work out alternative solutions before the process is finalized.

For many lenders, foreclosure is expensive and time-consuming. Because of that, banks are often willing to work with homeowners through options like:

Repayment plans

Loan modifications

Temporary forbearance

Payment adjustments

The earlier homeowners communicate with their lender, the more opportunities they typically have to find a workable solution.

Homeowners Have More Options Than They Think

Falling behind on payments can feel overwhelming, but it’s important to know that missing a payment or two does not automatically mean losing your home.

Today’s market gives many homeowners options that simply didn’t exist in 2008. Whether it’s restructuring a loan, creating a repayment plan, or selling the home before foreclosure becomes unavoidable, there are often multiple paths available.

And if selling becomes the best solution, working with a trusted real estate professional can help homeowners understand their home’s value and explore the best next steps.

Yes, foreclosure filings are rising compared to the unusually low levels we saw during the pandemic years. But overall foreclosure activity is still historically low, and today’s homeowners are in a much stronger equity position than they were during the 2008 crash.

This market isn’t showing signs of another housing collapse — it’s showing signs of normalization.

Comments